Introduction

by Mayra Portalatin, SFP, LEED AP O + M — As the need for Corporate Social Responsibility (CSR) takes hold in the corporate world, more organizations are looking to be more conscientious about their environmental footprint. At the same time, the world is on a financial rollercoaster, making our operational and capital expenditures on sustainable initiatives and energy efficiency even more challenging. That is, facility managers are being asked to help the organization make their buildings more sustainable (which requires some investment), while cutting costs to keep up with the struggling economy. So let’s add another to the many multiple hats that, as facility managers, we must wear. Time to put on the accountants hat!

Over the years, educational and professional development opportunities have allowed facility managers to arm ourselves with the tools needed to make a financial business case; but it is not always a simple task, nor one that we may feel comfortable doing. We may not use all of the tools available because in the past, we did not need that level of detail or complexity in making the business case. However, difficult financial times may require that we pull out all the stops to make the case for sustainability.

Tools for your Business Case

One of the most commonly used tools to make the business case for sustainability is the simple payback period (SPP). That is, how long before the investment pays off. It’s a quick way to evaluate a project’s economic feasibility and decide whether you need to look deeper prior to implementing an initiative. Although very easy to calculate, the calculation fails to account for what you gain after the initial investment is paid off. It also does not account for the time value of money (TVM). The TVM is a methodology for looking at the potential future value of a dollar invested at a known (or target) interest rate, or by looking at the investment rate required to reach a future target dollar value.

Another tool commonly used is the return on investment (ROI). Simply put, it is the “savings” generated by the investment over the initial cost, expressed as a percentage. Essentially it’s the inverse of the simple payback period. It is used to compare different initiatives. The higher the ROI, the better one initiative is over the other. However, it may have the same limitations as SPP if you do not account for the time value of money.

Life-cycle cost analysis (LCCA) is a financial tool that is used to compare two or more projects that are different with regard to scope and timing. In this process, you look at all the costs associated with an initiative, such as planning, design, construction, operations & maintenance, all the way to disposal. That is, you’re looking at the overall cost of your project from “cradle to grave”. LCCA requires more effort that SPP and ROI, but it can provide a more complete picture to make a more informed decision.

There are other tools that can be just as helpful as LCCA that take more into consideration for the analysis. Two of these are net present value (NPV) and internal rate of return (IRR). The NPV allows facility managers to determine the minimum rate of return on a project as well as compare the economic feasibility of several projects, while the IRR measures the profitability of an investment.

- Capitalization Rate = 8%

- 8-year Study Period

- Organizational minimum ROI = 15%

- No Rebates

- No energy cost escalations

- No differentials in lamp life

Using the Tools

Let’s look at one initiative with each of the tools. Let’s say we have a lighting retrofit project that we are considering. The initial investment on the lighting retrofit project is $50,000 to replace existing T-12’s for T-8’s. You have an estimated $10,000 in annual energy savings. How will each financial tool fare in helping you make a decision?

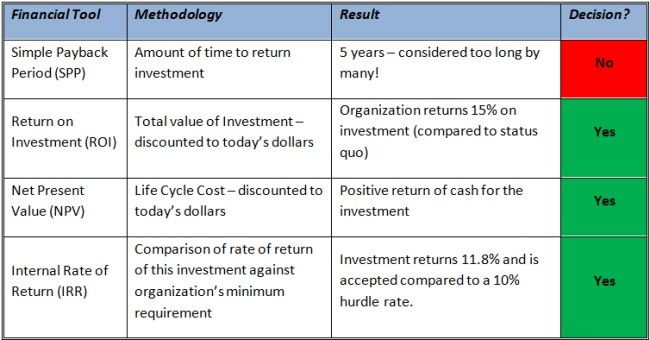

Simple Payback Period — In our example, the project will pay itself back within 5 years. The question you have to ask yourself, is a 5-year pay back acceptable to the organization? As most organizations are looking for shorter payback periods (typically between 1 and 3 years), the answer is probably, no. Another thing to consider in your decision making process is that it ignores $30,000 in energy savings after the initial investment is recovered (in years 6, 7 and 8).

Simple Return on Investment — As previously mentioned, simple ROI is the inverse of SPP (investment cost/annual savings), resulting in 20% for this project. While it is a positive return, the question remains, is this a worthwhile return on your investment? Typically the question can be answered by an organization’s accountant or chief financial officer (CFO). In this case, since the organization typically has a 15% on investment, an ROI of 20% would be acceptable. Since simple ROI does not account for the time value of money, many organizations use discounted ROI to determine the value of an investment.

Net Present Value — NPV calculations consider all cash inflows and outflows over the life of an investment and convert them all to the value of today’s dollar. In this case, energy savings would be considered cash inflows (as compared to the status quo, or keeping the T-12’s), and outflows would be the initial investment. In order to perform a NPV calculation, you need to know how your organization “values” money. In other words, if your organization could reinvest the same amount of capital you needed for your lighting retrofit in itself or another worthy investment, how much could it make? This is called the capitalization rate. It represents the minimum investment rate that your organization is seeking. Using the time value of money (NPV) and a capitalization rate of 8%, your net positive cash flow would exceed your initial investment by $7,466 – a good investment to make!

Internal Rate of Return — The IRR is that rate of return on a series of cash inflows and outflows that equal the present value of the investment (where NPV equals zero). It is the discount rate that makes the investment pay for itself over its service life. In our example, the IRR is 11.8% — a good return by almost any standards. The IRR is a measure of the project’s return on investment and needs to be compared to the organizations hurdle rate to determine if it has adequate value. The hurdle rate is the organization’s capitalization rate, plus any premium the organization decides to place on the rate of return to account for risk or additional profit. For the lighting retrofit in this example, the IRR of the project (11.8%) is compared to the organization’s hurdle rate (8% capitalization rate plus 2% “premium”), still making this a good investment by organizational standards (11.8% exceeds the 10% hurdle rate).

Summary

As you can see, the same project analyzed in different ways can yield different decision outcomes. If you had stuck to the SPP, you would have walked away from the project and $30,000 in savings after the investment had been paid off. Table 1 below summarizes our example and the different financial analysis outcomes.

The key to using these financial tools is to understand when to use which. But in the end, no matter which tool you use, understanding your organization’s accounting philosophy and methodology so that you can build your case for sustainability is a must for the wise facility manager.

Mayra Portalatin is a Civil & Environmental Engineer with over 14 years of consulting experience in building investigations ranging from condition assessments to sustainability audits. She has presented on the subject of sustainability and the built environment to property and facility managers in various venues including Greenbuild. Mayra is also an IFMA instructor for the Sustainability Facility Professional certification.