Posted by Johann Nacario — April 25, 2023 — Over the last decade, companies have been looking to the cloud as a way of accelerating the shift toward digital but were held back by inevitable change barriers that come with business transformation. The pandemic served as the ultimate wake-up call for organizations to take their information technology (IT) infrastructure to new heights and accelerate their timelines to become fully transformed enterprises. According to global real estate and professional services firm JLL’s new Global Data Center Outlook, the mass adoption of cloud computing and artificial intelligence (AI) is driving exponential growth for the data center industry, with hyperscale and edge computing leading investor demand.

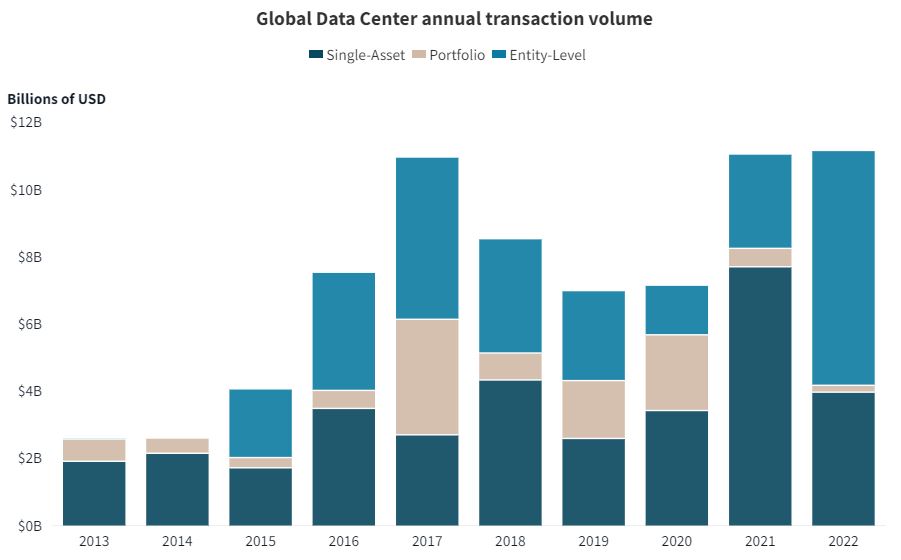

Graphic courtesy of JLL. Click to enlarge.

Andy Cvengros, managing director, JLL, remarked:

After the pandemic removed the four walls of the workplace, our new world of hybrid work has created an unprecedented need for digital technology. Employees are looking to their companies to create a seamless experience wherever they choose to work, requiring intelligent technology solutions to bridge the gap between the physical and the digital. As this reliance on digital technology increases, the data center industry is experiencing impressive growth and catching the eyes of investors and lenders as a strong, alternative asset class that has been relatively unimpacted by continued economic uncertainty.

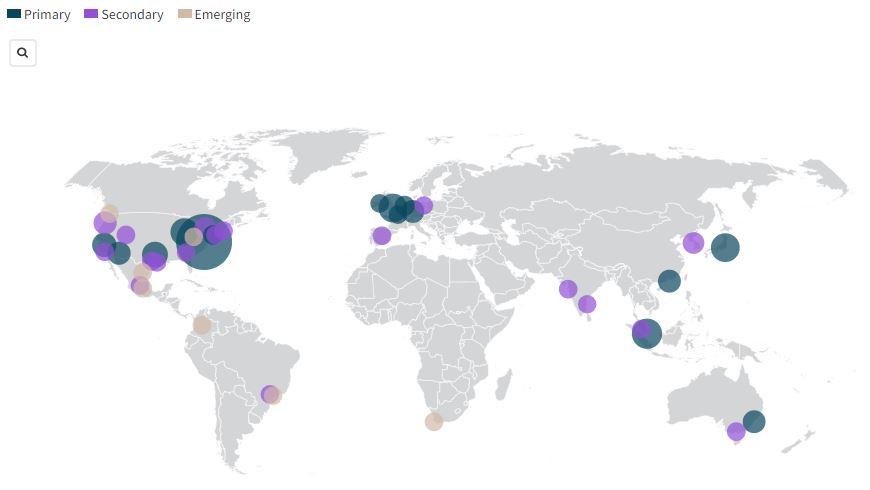

With internet usage almost universal, the need for more robust connectivity and innovative data storage solutions continues to drive high investor demand, where the global colocation data center market size is forecasted to grow 11.3% from 2021-2026. The U.S. is seeing strong appetite compared to other regions and accounts for 52% of all data center transactions from 2018 to 2022. Additionally, the U.S. had 1,633 megawatts (mw) of absorption in 2022 for the six U.S. primary markets: Chicago, Dallas-Fort Worth, New Jersey, Northern California, Northern Virginia and Phoenix. These markets also have 1,939 mw under construction.

Graphic courtesy of JLL. Click to enlarge.

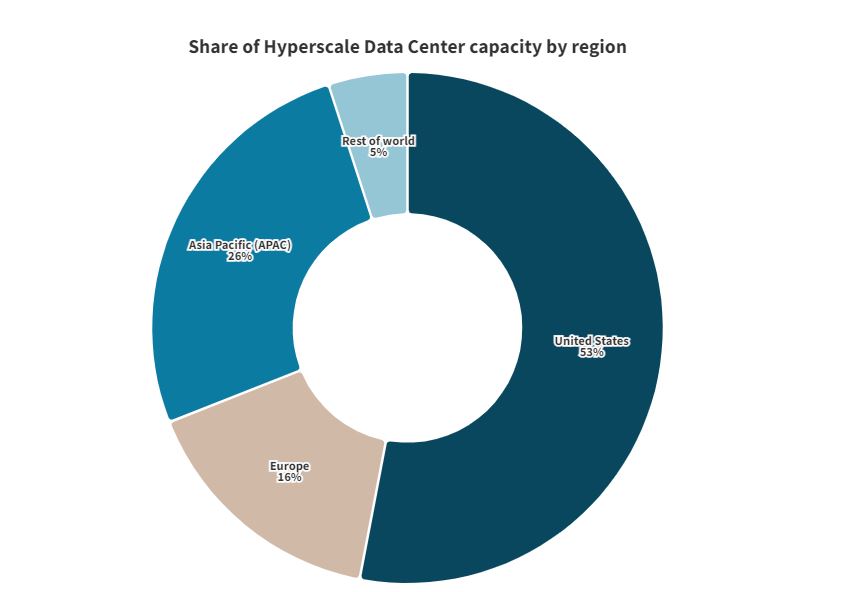

As the demand for digital IT infrastructure continues to increase, hyperscalers and edge are poised to be the fastest-growing segments of the data center industry. In fact, the hyperscale market is expected to grow 20% from 2021 to 2026, as more major tech companies look to meet surging demand for data processing and storage requirements. With 314 new hyperscale sites globally in development today, that number is expected to surpass 1,000 by the end of 2024 — up from around 500 sites just five years ago. Fifty-three percent of hyperscale capacity is in the U.S., according to Uptime Institute.

Graphic courtesy of JLL. Click to enlarge.

The goldrush of AI today is driving growth even further. Following the rapid development of AI tools like ChatGPT, the potential of generative AI to transform industries in 2023 is expected to accelerate demand for computing power in data centers. With AI offering increased data usage and computing efficiency benefits, half of all cloud data centers are expected to use AI by 2025.

Despite this strong demand, however, the skills shortage for high-tech talent will remain a challenge for the data center market’s continued growth. According to the Uptime Institute’s annual data center survey, nearly half of the workforce is approaching retirement within the next decade, and younger workers without the necessary technical skills are unable to fill new roles quickly enough to keep pace with sector growth.

As operators look to aggressively grow and deepen their bench of expert talent to avoid an industry-wide talent shortage, there will be increased focus on mass training programs for high-tech jobs. Government instituted programs will be to key keeping the data center talent pipeline full, including most recently with the CHIPS for America Act that offers grants and loans to help boost the education pipeline across the technology ecosystem, including data centers.

Matt Landek, managing director, Data Centers & Telecom, Work Dynamics, JLL said:

At a time when our increasingly digital world is exploding with demand, data center operators are discovering that younger generations pose an entirely new recruitment challenge. To help futureproof the industry and mitigate the labor pipeline drying up, scaling robust training and recruitment programs will be key in 2023 and beyond to build a stronger, more diverse pipeline of young talent.

The report also explores corporations and governments focusing on ramping up efforts to close the gap between environmental commitments and action in the race to net-zero. The data center industry is facing increased pressure for more transparency of climate mitigation efforts and has been working toward more sustainable operations. Being one of the most energy-intensive building types, data centers collectively account for approximately 2% of the total U.S. electricity use, and, at the end of 2021, global data center energy consumption reached 190.8 terawatt hours — 2.2 times more than 2020.

To incentivize a more transparent and standardized approach toward sustainability, climate legislation momentum and self-regulatory initiatives are driving technology improvements and new sources of power. From the Inflation Reduction Act that extends tax credits for sustainable energy sources to the SEC proposing new climate-related disclosure requirements for public companies. First-mover operators who react swiftly to improve efficiency with both energy and water usage stand to benefit as environmental impacts remain top-of-mind for leading companies and investors.

Find more results from the new Global Data Center Outlook at JLL.